As the COVID-19 crisis accelerates, local governments are in a precarious position. Like other periods of economic strain and distress, government leaders must evaluate the trade-off between maintaining essential public services and instituting austere measures to ensure long-term financial sustainability.

INTRODUCTION

Over the record-length economic expansion following the Great Recession, local governments had the opportunity to build up reserves that could weather a downturn. Now that the downturn is upon us, finance officials must determine how sufficient those reserves are in responding to their municipality’s needs, and what other fiscal or strategic actions may be required to completely respond to every facet of the pandemic.

Ultimately, the exercise likely revolves around several related questions:

- Without making any substantial adjustments, how long can existing reserves last?

- What menu of options exist, for either raising revenues or reducing expenditures, and when must they be employed to make a meaningful difference?

- After employing these measures, can the government last financially, or must permanent budgetary changes be enacted?

- If the local economy does not return to normal in the near or medium term, due to permanent business closures, continued unemployment and even foreclosures, what does that mean for the structural position of the budget?

Governments will need to determine how they can continue to best serve their communities given the finite resources at their disposal.

Nobody wants to curtail or diminish services, or even potentially increase tax rates during difficult economic times, but without proactive responses to the current crisis, communities will experience far greater disruption to government services down the road.

**Unlike the Great Recession, the current economic landscape did not originate from a ‘financial crisis’, but the reality of the crisis facing local governments is in no uncertain terms a financial one**

As a best practice, it is recommended for municipalities to do a long-term projection, a picture of their financial future which projects historical trends, current budget, and community goals.

The baseline represents the current state and trajectory, governed by the largest revenue and expense drivers in the budget, and their respective anticipated future growth patterns. Holistically, the baseline projection is like the diagnosis your doctor gives you after a physical. It reflects your current condition, given the major underlying factors.

Now, due to the closures, shutdowns, and market crash caused by the COVID-19, local governments need to adjust to a new baseline – at least for the immediate future. Many major revenues streams are about to hit a shock while municipalities are still seeking answers around how various expenditure components will normalize in the short-term.

Some or all of these may need to be reflected in the next budget, if not incorporated as a revision to the current one. Not only is the immediate financial impact tangible, but many of these near-term adjustments may end up being structural and persist in some form for years to come.

Understanding ‘the new financial normal’ is a crucial first step to ensuring that the ramifications of every proactive decision are fully analyzed and understood within the full context of the government’s current financial reality.

REVENUE ANALYSIS & IMPACT

One of the most immediate impacts that will occur is a drop in revenue and, depending on the individual tax, fee, program, and other revenue makeup of the government, this impact may vary both in terms of severity and duration.

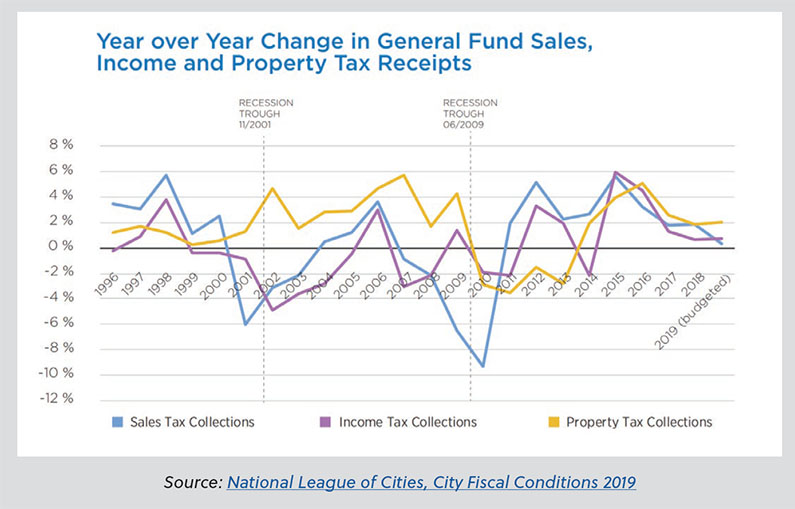

(though this can vary somewhat across states) which have a high level of resiliency and tend to lag other economic indicators during a downturn.

Property values take time to adjust to economic conditions mainly due to the time it takes to takes to reassess each property, which is what would ultimately drive property taxes down.

Furthermore, in certain jurisdictions reassessments are done on a more rigid schedule, so the impact may necessarily be amortized over several years. Even during the Great Recession, which was driven substantially by a housing bubble, local property tax receipts never decreased by more than 4% year over year, and a decline was not experienced until 2010.

A decline in sales tax revenue, on the other hand, will be much more immediate. In this particular crisis, as people quarantine and increasingly limit their economic activity to absolute essentials, local economies – and therefore sales tax revenues – are going to take a substantial hit.

Sales tax is always a highly volatile tax stream, as individuals can adjust their spending behavior largely on an immediate basis. In the case of the current Coronavirus pandemic, it may be possible that a relatively quick recovery occurs, and the most substantial impacts will be seen in the current and next budget year.

However, depending on the local economy, particularly for businesses under the ‘non-essential’ umbrella that cannot operate virtually, permanent business closures will leave a longer lasting effect.

For localities that are not able to levy a local sales tax, this impact may be seen indirectly from intergovernmental revenues through the state, where almost all states derive a substantial portion of their revenues through sales tax receipts.

A limited number of states enable individual cities, towns, townships, counties, etc., to levy a local income tax. Pennsylvania and Ohio are two states that allow this, making income tax a meaningful source of revenues that they can rely upon during economic hardship. Though not as immediate an impact as sales tax, income tax collections can respond to economic changes reasonably quickly.

With jobless claims surging to almost 17 million as of April 9th, according to the department of labor, governments dependent on income tax may see near term declines. Substantial variability may impact all income-tax dependent municipalities ability to recover, as it is highly uncertain how, and in what time-frame, income tax revenue returns to normalcy.

For other traditional governmental revenue sources – licensing and permits, fines and fees, charges for services, among others – the economic decline will have a downward pressure.

Reduced economic and social activity, not with-standing the ability to process and collect revenues due to virtual work environments, may lead to declines. Local governments should look at the impact the virus is having to their local economy and understand specifically what the potential magnitude of change will be in each of these sources. Reviewing trends from the last recession will be a useful guide for how these other revenue streams behave.

Any tourism related taxes, such as hotel and transient occupancy taxes, certain excise tax-es, and other taxes related to consumption by individuals visiting the community will experience a massive blow. With social distancing becoming increasingly common and more businesses limiting themselves to only essential travel, tourism and luxury purchases are at a virtual standstill.

It is unclear how long the residual effects of COVID-19 will persist, but if recessionary trends continue beyond the near-term and social distancing does not flatten the curve of new cases, these effects may be longer lasting than the crisis itself.

States and the federal government have initiated emergency relief and support bills to help bolster the resiliency of local governments, among other economic actors, across the country. At the federal level, a $2 trillion bill recently passed to provide a massive stimulus which will have both direct and indirect impacts to municipal entities.

state and larger local governments in the form of direct aid to stem the tide of revenue loss.

Expenditure Analysis & Reduction

Local governments will need to determine what an appropriate balance is regarding expenditure reductions that sufficiently mitigate the impact of revenue loss while maintaining stable levels of public services.

Local governments should know what proactive measures and financial maneuvers they have at their disposal, and collectively develop an under-standing of when and where to implement them.

The sooner the various financial options are realized, by key municipal stakeholders, the quicker and more proactive those stakeholders can utilize their tool set to steer their community on the best available path forward.

Expense Reductions through Personnel Costs

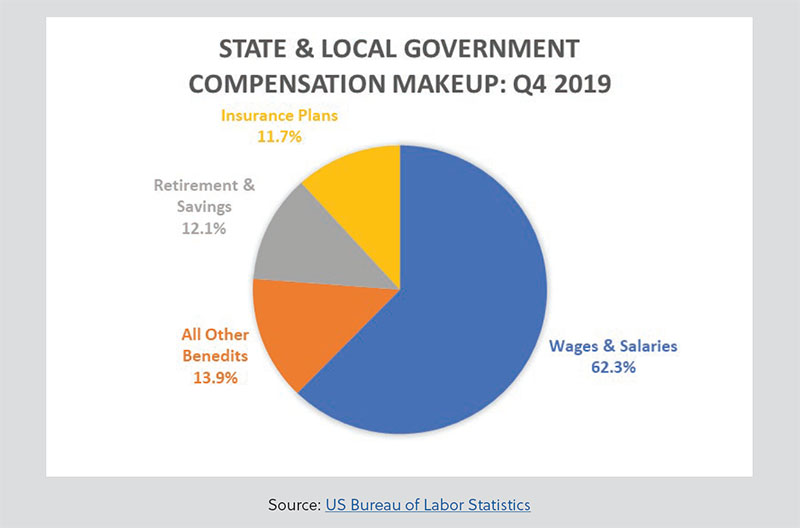

Personnel costs are a common malleable expense category governments can use to positively alter its future financial condition.

Utilizing furloughs, where a worker experiences a temporary leave – in this case without pay – may allow the government to drive down personnel costs, which are typically the overwhelming cost component of government operating budgets.

Making use of furloughs in departments that may be experiencing decreased demand due to the nature of the virus, such as parks and recreation, can help reduce costs without diminishing public services.

Hiring and wage freezes, to the extent permissible based on labor contracts and collective bar-gaining, can help contain employee costs. Not replacing retired workers and allowing attrition to reduce workforce size (and likely average salary level) is a tactic, though based on timing of retirements this may not be able to provide immediate relief. Reductions in work hours – both in terms of matching staffing to current public demand and balancing the needs of the public with the current financial reality – may drive down overtime and other fringe benefits.

To the extent that contracted services are coming up for bid, there may be enough downward pressure for these services to be reestablished at a lower cost than previously anticipated.

As a more severe measure, layoffs are a potential option. For this, and any other option within the list of ‘last resort’ measures, decision-makers should evaluate under what conditions they should consider utilizing layoffs. Having the conversation earlier on can help build some level of understanding and consensus for such difficult decisions.

Other levels include delaying of maintenance and repair initiatives. Forgoing, for now, equipment replacement, technology upgrades, etc. can provide much needed financial capacity in the near-term, but of course these costs do not go away forever, and may actually come back in the form of much higher costs later on, depending on the length of the delay and the severity of the maintenance required.

In other areas, expenditures may actually experience an upward pressure. Government entities, both public and quasi-public, have a tremendous amount of social pressure to not exacerbate the situation for individuals currently in dire straits.

For governments that maintain Enterprise Funds that deal with public utilities, this comes in the form of increased expenditures by not shutting off water and sewer services despite late or non-payments (though in residential communities, this may be offset by increased overall usage from individuals now working from home).

Though certain government services, as mentioned, may experience a decrease in demand and therefore a decrease in cost, other areas such as human services and public health will have an increase in need during the COVID-19 pandemic.

Expense Reductions through Pension Liability

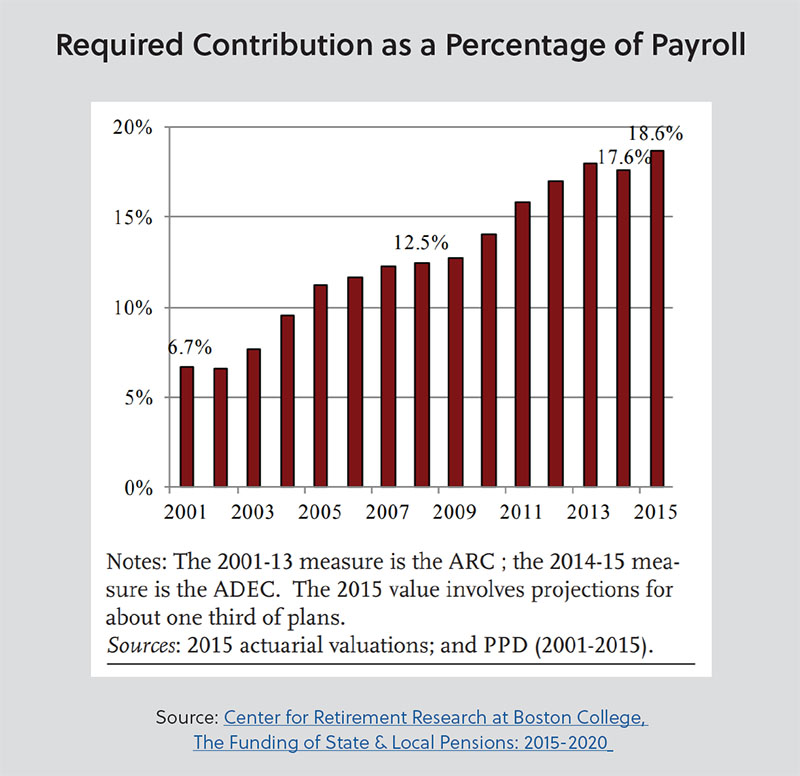

An expenditure reality that will manifest over time is an increase to pension contributions. With the massive decline in equity markets over the past several weeks, the employer contributions required to maintain the same path to full funding will slowly increase.

The vast majority of public pension plans utilize a multi-year ‘smoothing’ of assets, which amortize gains and losses over some designated period of time (generally 3-7 years) such that funding requirements for the public employer do not move wildly year to year. The losses that are likely to be incurred this year – assuming the stock markets do not experience a recovery that essentially eliminates those losses – will begin to appear in the smoothed actuarial valuation of assets.

The reported funded ratio may be much lower after the actuarial valuation of assets are realized, resulting in a higher level of contribution needed from public employers to make up for losses caused by the pandemic market crash. Depending on the asset class makeup of the fund, the current level of contribution, and the current funding health of the plan, the magnitude of additional funding required can vary. Given the current funding position of many state and local plans, it is likely a meaningfully substantial increase in funding requirements will be experienced for years to come to keep these plans on a path to full funding.

Debt & Capital

Capital projects are generally a ‘discretionary’ component of governmental costs, at least to the extent that their timing and method of delivery have some discretionary variability. Unlike non-discretionary operating costs, i.e., police force and fire safety personnel, public officials can evaluate and prioritize capital projects that relieve real financial strain.

Delayed infrastructure upgrades can entail a higher cost burden down the road; e.g., not paving the roads today means they will be in worse condition and be more cost intensive if you wait to pave until a later date. In some cases, avoiding these delays may not even be an option in areas where non-essential construction has been curtailed.

As revenues decline, and municipalities must dip into their reserves, there is a rapid exercise going on across the country where governments are trying to determine how long their current level of fund balance may last under ever-changing pandemic conditions.

Whether or not various measures are taken to reduce expenditures, there is only a finite period of steep revenue decline that can occur before available cash is exhausted.

Short-term borrowings, which are sometimes used by local governments to bridge the gap for the timing of bond proceeds, property taxes, or other major tax receipts, can extend the life of available reserves.

When evaluating this as an option, government officials should be aware of the volatility in the municipal market, where access to capital markets in general have been in flux and not as dependable or stable as they have been under normal circumstances.

Other mechanisms involving debt include restructuring, which takes principal payments currently scheduled to amortize in the near-term and re-amortize them at a later date. Though providing immediate relief in terms of short-term debt obligations, this option has the potential to come at a substantial cost over the long term.

In all cases related to debt financing options, municipal issuers should seek the advice of municipal advisors as to what may be suitable for any particular situation.

Synopsis Wrap-Up

The road ahead will be a monumentally challenging one. With the landscape so fundamentally different, and continuing to develop in different ways, there is a substantial amount of change and uncertainty that lie ahead for local governments.

Understanding what the possibilities of short- and long-term financial impacts are will be the first step in charting a course of proactive, corrective action. Though there is a nature of immediacy to the exercise, municipalities should be projecting their financials past the next several months to avoid pursuing a trajectory that could negatively impact their constituents and communities.

With so much up in the air, and so many of the significant variables in flux – i.e. pandemic length, economic recovery timing, federal and state aid packages – the time to begin that dialogue and plan out the future is now.

This material is for general information purposes only and is not intended to provide specific advice or a specific recommendation. This email content is being provided by PFM for educational and informational purposes only, and may be construed as advertising under applicable U.S. or state laws. PFM can be contacted at 1735 Market Street, 43rd Floor, Philadelphia, PA 19103, or by telephone at 215.567.6100. For important disclosure information, please go to pfm. com/disclosures.